The Only Options Trading Guide a Beginner Will Ever Need (The Basics from A to Z)

So you want to learn all well-nigh options, but you’re worried well-nigh getting tumbled or overwhelmed? We’ve got you covered.

You might have heard that options trading is a unconfined way to make spare income if you’re working a full time job. Or perhaps you’re looking to enhance the returns of your investment account.

But the problem is that you just find options trading troublemaking and mysterious and don’t really know how to get started.

Well the reality is that options are really easy to understand. All you need to do is take a few minutes to learn some simple concepts and then a whole new world of trading will unshut up to you that you probably never knew existed. It’s a world where you don’t plane need to pick the direction you think a stock is headed to make money on the options of that stock.

And we should know, we’re one of the top proprietary trading firms in the world, and the 50 professional traders on our trade sedentary here in New York City use the strategies that we’ll be teaching you in this vendible all of the time. So don’t worry, we can unravel this lanugo for you. It’s not that hard.

Now in this article, you’ll be hearing a lot well-nigh two key terms that are at the cadre of options trading: Call Options and Put Options. And while options are traded on lots of variegated kinds of assets, in this vendible we’re going to be focusing on what is meant by undeniability and put options on stocks and undeniability and put options on indexes.

Call Options On Stocks

So what is a undeniability option on a stock exactly? A undeniability option is basically a bet. The proprietrix of the undeniability option is making a bet that the stock is going to go up vastitude a unrepealable price which is known as the “strike price” of that option. For that bet he pays what is tabbed a “premium” equal to 100 times the price of the option. The undeniability seller is the one taking that bet and receiving that premium.

If the undeniability proprietrix is right, he is entitled to buy 100 shares of the stock at the strike price of the option, plane if the stock has moved much higher than that price. If the undeniability proprietrix is wrong, the undeniability seller pockets the premium that the proprietrix paid him for taking that bet.

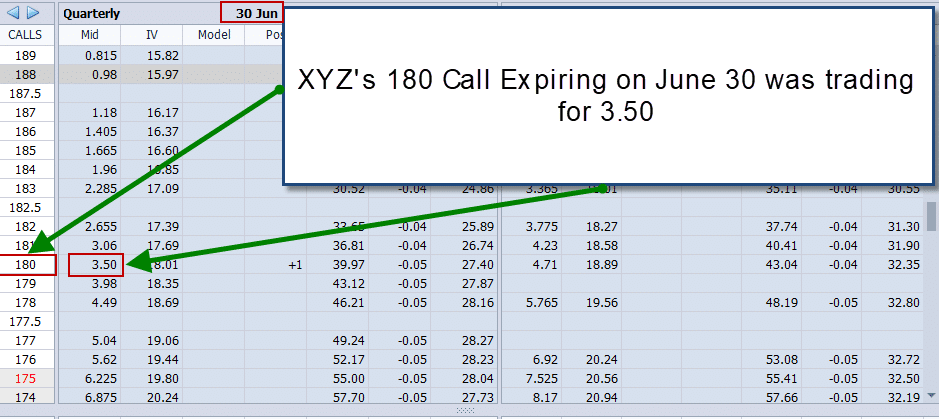

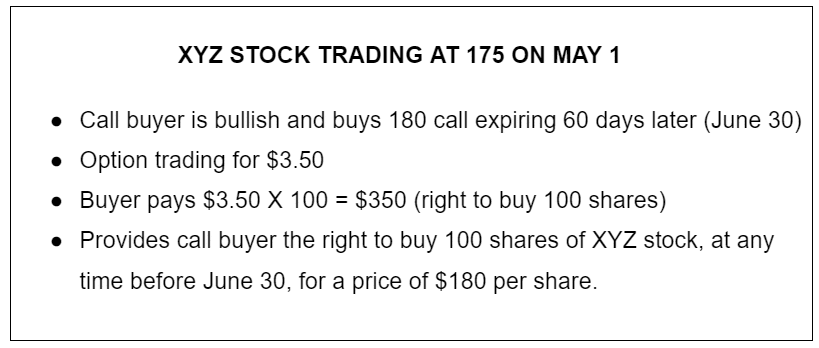

So for example, let’s say that on May 1st, XYZ stock is trading at a price of $175. Now, let’s say that a trader believes that XYZ stock will rally. Resulting with his opinion, he might decide to buy the 180 undeniability which expires on June 30th, well-nigh two months later.

Now, options are misogynist in what are known as “options chains” that elapse on variegated dates in the future. So in order to buy the 180 undeniability for XYZ stock expiring on June 30th, he goes into the section of his broker’s trading software where he can find XYZ stock options and he pulls up the June 30th chain. And as you can see, he found that on that day, the 180 undeniability was trading for $3.50:

The premium for that undeniability is $3.50 but remember he pays 100 times that price, or $350 for the right to buy 100 shares of that stock at 180 regardless of how upper it goes.

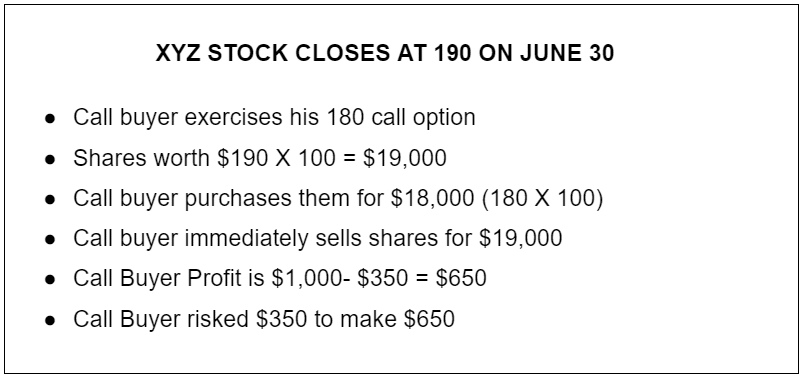

If the stock rallies to say, 190, then he can exercise his undeniability option, buy the shares for 180 and then turn virtually and sell them immediately for the market price of $190, making ten dollars on each of his 100 shares for a proceeds of $1,000 on those shares. Deducting the $350 forfeit of the option nets the undeniability proprietrix a profit of $650. So the undeniability proprietrix risked $350 to make $650, a reward that is a little less than twice the risk.

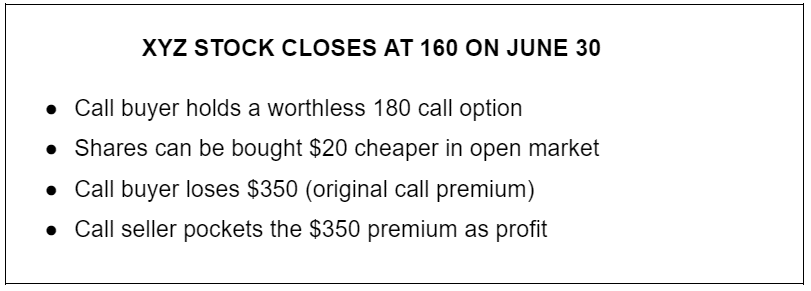

On the other hand if the stock sells off to say 160, then on November 16th, the options seller, the one who took the risk, gets to simply pocket the $350 premium he received for the undeniability buyer’s bet. In other words, that option expires worthless.

Why is it worthless? Well if you have an option to buy shares at 180 but the stock is trading for 160, who is going to exercise that option to pay $20 increasingly than anyone else has to pay for the same shares? No one, obviously, and so the option has no value and the option price closes at zero on the option’s expiration day.

Put Options On Stocks

Now a put option on a stock is basically the opposite bet. The proprietrix of the put option pays a premium in this specimen (again, equal to 100 times the price of the option) to the put seller, making a bet that the stock will go lanugo vastitude the strike price of the put option. And again, the put seller is the one taking that bet.

In the specimen of a put, if the put proprietrix is right, he gets to sell, to the put seller, 100 shares of a stock at the strike price of the put option, plane if the stock has moved much lower than that price. If the put proprietrix is wrong, and the put expires ABOVE the strike price of the put option, the undeniability seller just pockets the premium that the proprietrix paid him for taking that bet, as profit.

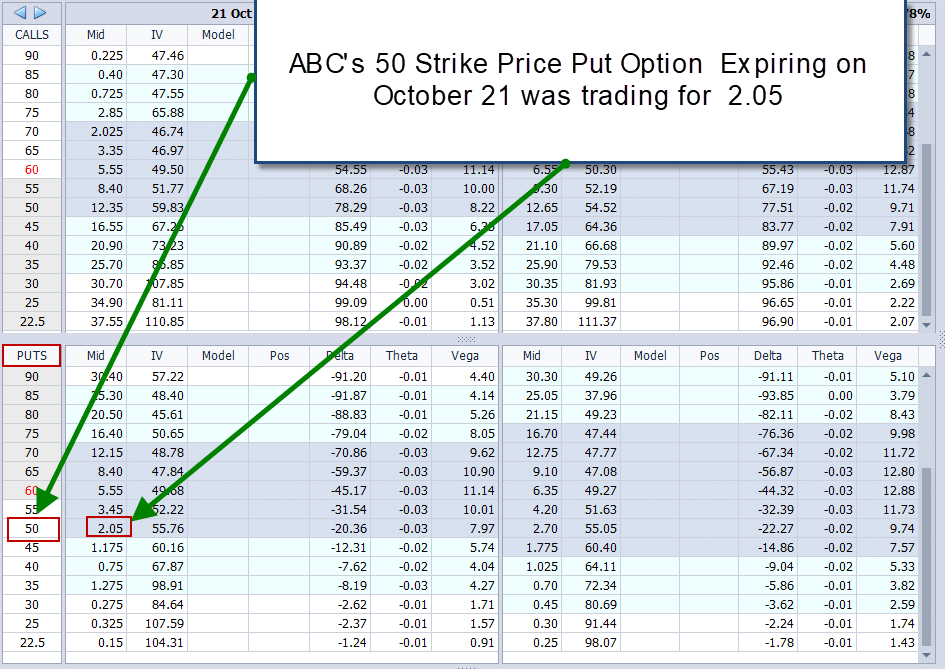

So for example, suppose that ABC stock is trading at virtually 60 on August 1. Suppose a trader owns 100 shares of XYZ and wants to buy protection for those shares so that if the stock goes lanugo unelevated 50 surpassing October 21, he can sell those shares for 50 no matter how low the stock goes. In that specimen then he could buy the 50 put for $205—the 2.05 options premium times 100–representing his 100 shares.

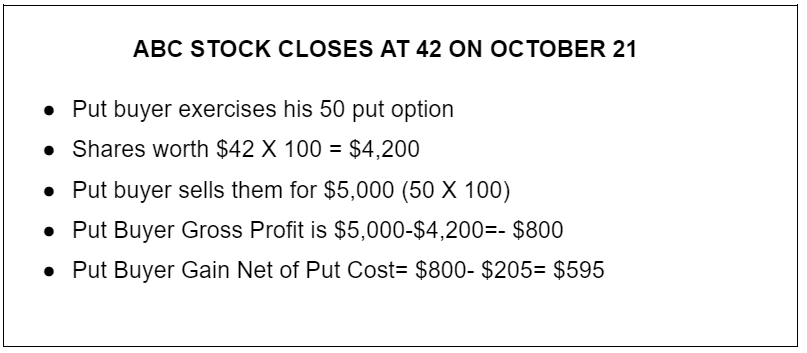

Now, if the stock closes at 42 on October 21, then he can exercise his put and sell the shares for 50, which is 8 points increasingly than they are worth on the unshut market. So he saved $800 on a gross basis–$8 for each of his 100 shares. Factoring in the forfeit of the put, $205, the put proprietrix is $595 largest off than had he never bought the put.

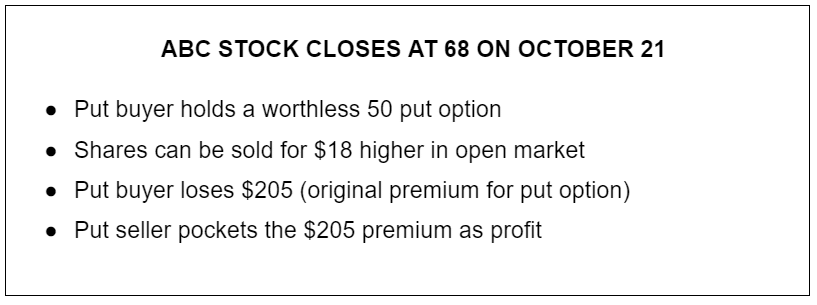

On the other hand, if XYZ rallies from its current price of 60 and closes at 68 on October 21, then the one who took the bet, the put seller, gets to just pocket that premium considering the 50 put option, again, expires worthless. Why? Well who would want the right to sell shares at $50 when in the unshut market he can get $68 for those shares? Obviously that right is worthless, and so the option has no value and it simply expires worthless.

On the other hand, if XYZ rallies from its current price of 60 and closes at 68 on October 21, then the one who took the bet, the put seller, gets to just pocket that premium considering the 50 put option, again, expires worthless. Why? Well who would want the right to sell shares at $50 when in the unshut market he can get $68 for those shares? Obviously that right is worthless, and so the option has no value and it simply expires worthless.

Stock options at Expiration

When a stock option expires, your usurer will take a squint at the option and determine whether it has any value or not. If it’s a undeniability option, and the stock price at latter is “out of the money” it ways that the stock is sealed at a price lower than the strike price of the undeniability option in which specimen the option expires with no value and just disappears from your account.

But if a stock closes at a price ABOVE the undeniability option’s strike price, then your usurer will automatically execute that option for you in which case, for each undeniability option you own, you’ll receive 100 shares of that stock for which you’ll have paid the strike price of the option for each share.

So for instance, if you own a $95 strike price option for XYZ stock which closes at $98 on the day the option expires, your usurer will pay out of your worth $9,500 ($95 per share X 100 shares) to the undeniability seller and the undeniability seller’s usurer will then unhook to your worth 100 shares of the stock worth $9,800 (the $98/per share market price X 100 shares).

In the flukey specimen where the stock closes EXACTLY at the strike price of the stock on the day it expires, meaning the stock expired “at the money”, then the usurer will elapse your option with no value considering there’s no purpose in exercising the undeniability option to get shares of exactly the same value.

Stock options on puts are the word-for-word opposite. If the stock closes below the put’s strike price then 100 shares of that stock will be sold from your worth and you’ll be paid the put’s strike price for each of those shares, regardless of how low the stock’s latter price was on the day the put option expired.

It’s moreover important to realize that stock options are often “American Style Options” meaning that an probity put or undeniability option can be exercised at any time from the moment you buy it until it expires. That’s an important stardom because, as we’ll get into later, some options can’t be exercised until they expire. Those kinds of options are known as “European Style Options”.

In any event, if an probity option expires, your usurer will automatically exercise it if it has value as we just explained in the previous examples.

What’s the difference between owning stocks and owning options?

Aspect |

Stocks |

Options |

|---|---|---|

| Definition | Ownership shares in a company. | Contracts that requite the option proprietrix the right to buy or sell a stock. |

| Rights | Shareholders have ownership and voting rights. | Option holders have no ownership or voting rights. |

| Expiration | Stocks don't expire, they unchangingly have some value if the visitor is perceived by investors to have value. | Options have an expiration stage and the owner or the owner’s usurer must execute or sell the option surpassing it expires to get any value for it. |

| Dividends | Shareholders may receive dividends if the visitor pays. | Option holders don't receive dividends. |

| Risk | Limited to the value invested in the stock. | Limited to the premium paid for the option. |

| Profit Potential | Unlimited, based on the stock's performance. | Unlimited on the upside with much greater return potential than stocks due to the inherent leverage of options in the specimen of a call, Limited only if the stock’s value falls to zero in the specimen of a put. |

| Leverage | No leverage, you buy shares at their market value. | Leverage is inherent in options trading, magnifying gains and losses. |

| Strategies | Buy and hold, short selling. | Various strategies like ownership and selling calls, covered calls, spreads, straddles, strangles, etc. |

| Flexibility | Limited flexibility in terms of strategies. | More flexibility in constructing ramified strategies |

| Complexity | Straightforward ownership and selling process. | Can be increasingly ramified if options strategies involving multiple options are traded at the same time. |

Okay, so now that you know how options work on stocks, let’s move to how options are used to make “bets” on unshortened probity indexes such as the S&P 500 or the Dow Jones Industrial Average.

But surpassing we do that, if you’re really interested in options trading you need to trammels the self-ruling intensive workshop we’re currently running. In it you’ll discover:

— The unique options trick that allows you to make money while you wait to buy stocks or ETFs at the price you want (one of Warren Buffett’s secret techniques).

— The options income strategy that allows you to make resulting money whether the market goes up, down, or sideways.

— How to make money on a stock or alphabetize trade plane if you’re outright wrong on the direction (the stock can do the exact opposite of what you predict, and you’ll still win).

It’s 100% free, so reserve your options workshop seat now.

Call Options On Indexes

Similar to stock options, a undeniability option on an index is a bet on an unshortened index. The proprietrix of the alphabetize undeniability option pays a premium (again, 100 times the option’s price) for a bet that pays off if the alphabetize gets vastitude the strike price of the call. The undeniability seller is the one who takes that bet. If the undeniability proprietrix is right, he gets a cash payment of $100 for every point that the alphabetize exceeds the call’s strike price on expiration day. If he’s wrong, the seller pockets the premium, just like with stock options.

The proprietrix of an alphabetize put option gets a payment of $100 for every point the alphabetize is below the put’s strike price on the day it expires. If the put proprietrix is wrong, the seller, again, just pockets the premium.

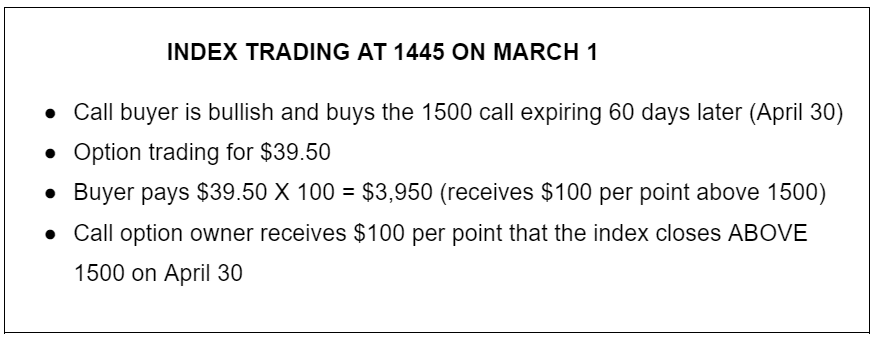

So for instance, suppose that an index’s value on March 1st is 1445 and the trader becomes bullish on that index. And suppose that the 1500 call, 55 points whilom the current price, which expires on April 30, 60 days later, is trading for $39.50. Well in that case, if he wants to make a bullish bet by purchasing the 1500 call, he has to pay 100 times that, or $3,950.

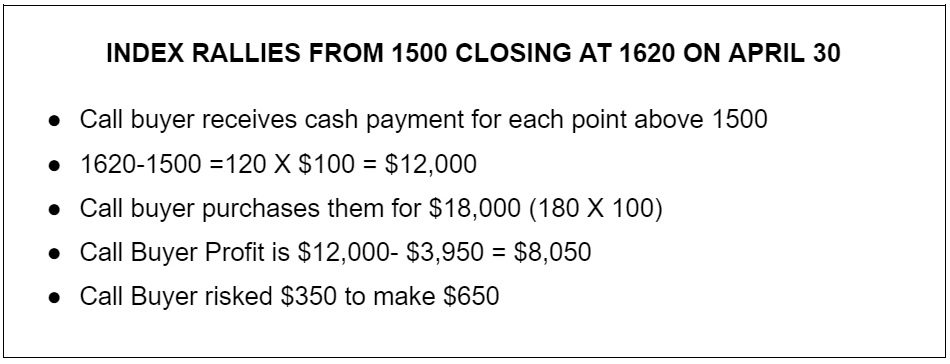

If the alphabetize rallies to vastitude 1500 by expiration day, to say 1620, then the undeniability option seller will have to pay the owner of that undeniability $100 for each point whilom 1500. In other words, the undeniability seller owes the proprietrix $12,000. And his profit is the $12,000 mazuma payment minus the original $3,950 forfeit of the option for a net profit of $8,050.

If on the other hand the alphabetize sells off to 1400, then the undeniability option has no value, the undeniability seller owes nothing to the undeniability proprietrix and therefore the undeniability expires worthless and the undeniability seller pockets the $3,950 that he was originally paid.

Put Options On Indexes

Put options on indexes are the word-for-word opposite of alphabetize undeniability options. Alphabetize put options only pay off if the alphabetize closes BELOW the strike price of the put option.

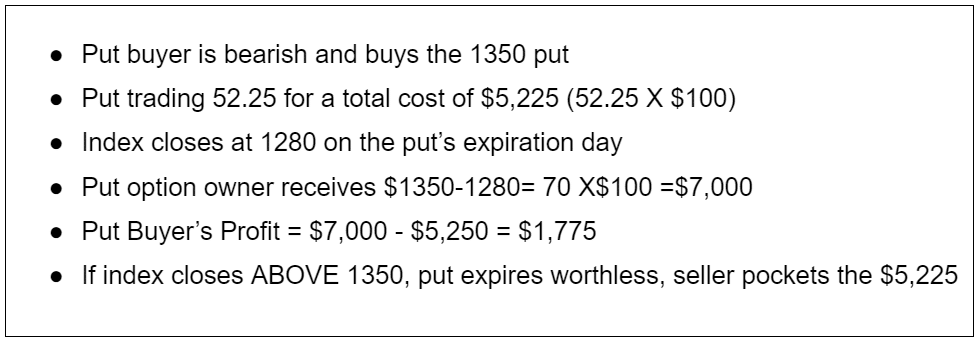

So let’s say that an alphabetize is trading at 1425 and you buy the 1350 put for $52.25, costing you $5,225. If the alphabetize sells off to 1280, then the put proprietrix owes the put seller $7,000 which ways that you’d make a profit of $1,775 without deducting the $5,225 put option cost. On the other hand, if the alphabetize closes ABOVE 1350 on the day it expires, the put expires worthless and the put seller, again, just pockets the premium.

Index Options at Expiration

Since you can’t own an alphabetize (you can only own shares of the stocks of its components), alphabetize options are “bets” that pay off in cash. In other words, alphabetize options are “cash settled” at expiration. If you own an in the money alphabetize undeniability your usurer will automatically exercise that option by retrieving from the undeniability seller the $100 for every point that the alphabetize sealed whilom the call’s strike price.

So for example, if an alphabetize closes at 3180 and you own a 3150 undeniability option on that index, your worth will automatically be credited with $3,000 considering the option expired 30 points in the money and therefore you’re entitled to 30 X $100= $3,000 in mazuma for “winning” that bet. However , if the alphabetize closes unelevated the call’s strike price on the day it expires, the option simply disappears with no value.

The word-for-word opposite is true of alphabetize put options. If the market closes below the put option’s strike price your usurer will credit your worth with $100 times the number of points the alphabetize sealed unelevated your put’s strike price.

How often can I make options trades?

Options elapse periodically and for each expiration stage the major options exchanges offer “options chains” for the options of that windfall expiring throughout the year. When in the day, the major exchanges only offered options expirations once a month, which expired on the third Friday of each month.

But in the first decade of this century the major options exchanges started to offer options villenage wideness a large swath of stocks and indexes which expire every Friday. Eventually unrepealable indexes (such as the SPX and NDX indexes) and the mart traded funds based on those indexes (such as SPY and QQQ) introduced daily options expiration dates.

The options market over the years has created a vastly greater number of opportunities to trade options contracts than when they first became publicly misogynist in the 1960s, giving traders an incredible opportunity to be increasingly targeted and granular in their trading strategies.

How are Options Priced?

Call Option Prices:

If you buy 100 shares of a stock and the stock goes up $2, it’s pretty obvious that you’ve made $200 on that stock. But if you own a undeniability option on a stock and the stock goes up $2, how much money do you make?

Well the true wordplay to that question is, “I don’t have unbearable information to wordplay that question”. And that’s considering a call option’s price will transpiration differently depending upon three variegated factors:

1. Strike Price: How far is the strike price of the option from the current trading price of the stock? Is it 20% whilom the current price? Is it 1% whilom the current price? Is it unelevated the current price?

For undeniability options the higher the strike price, the cheaper the option. That’s considering the higher the strike price, the less likely that the stock will reach that price surpassing the option expires and so the market doesn’t value the opportunity to buy at that price surpassing expiration as very valuable, considering it’s not very likely.

2. Expiration: How far into the future does the undeniability option expire? Does it elapse tomorrow? Does it elapse in a month? Does it elapse in a year?

The farther out in time the call’s expiration is, the higher its price will be. A later expiration allows the stock’s price spare time to reach that price and so the market values that undeniability option increasingly than an option at that same strike price, but less time to reach it.

3. Volatility: How volatile is the stock’s price? Is it the kind of stock that has huge swings in price, or is it relatively stable? Volatile stocks have price spikes and price drops that are much increasingly violent and frequent than low volatility stocks.

A volatile stock is increasingly likely to trigger a undeniability option, reaching it surpassing or at expiration than a low volatility stock which tends to grind up (or down) in a slower and increasingly orderly way, so volatile stock undeniability options will be increasingly valuable than their counterpart options on less volatile stocks all other things stuff equal.

All of these factors can be summarized in this table of undeniability option pricing:

Call Options Pricing |

Lowest Priced | Higher Priced | Highest Priced |

|---|---|---|---|

| Strike Price | Way whilom Stock Price | At or near strike price | Way unelevated stock price |

| Expiration | Very soon | Moderately far into the future | Far out in time |

| Volatility | Low | Moderate | Substantial |

Put Option Prices:

Once you understand undeniability prices, put prices wilt really easy to understand. And that’s considering put price valuations only differ from undeniability prices in one respect. If the stock to which it relates goes down, then, all other things stuff equal, the put prices goes up. Why?

Well let’s think of an example. Suppose that a stock is trading at $75/share and you buy a 70 put for that stock? Well if the stock goes lanugo to 71, then the put price, all other things stuff equal, will go up considering the chances of that put having value on the day it expires, which would be at any price unelevated 70, have obviously just increased if the stock went from 5 points whilom the option’s strike price to 1 point whilom the option’s strike price.

And that’s considering the value of having a contract, a put option, that gives you the right to sell your shares at 70 plane if the stock goes to 40 obviously just went up if the stock has downward momentum and may go farther. No matter how low it goes, that put option allows you to have certainty that you can get at least $70 per share for the shares.

So other than moves in the price of the stock, every other speciality of put and undeniability pricing are the same. Just as with calls, the farther out in time the option expires, the increasingly price you’ll get for the undeniability option. And just as with calls, the increasingly volatile a stock’s price is, the higher the put’s price will be. And so put pricing can be summarized in a very similar table as the undeniability option summary we gave you earlier:

Put Option Pricing |

Lowest Priced | Higher Priced | Highest Priced |

|---|---|---|---|

| Strike Price | Way unelevated stock price | At or near strike price | Way whilom stock price |

| Expiration | Very soon | Moderately far Into the future | Far out in time |

| Volatility | Low | Moderate | Substantial |

By the way, if you’re enjoying this vendible but want plane increasingly in-depth options education that covers all the nuts but moreover gives you specific, practical strategies that you can hands employ yourself (even if you’re a beginner), throne over to OptionsClass.com. It’s completely free.

Why Buy Stock Options Instead of Stocks?

There are similarities to ownership stock options versus stock trading. Every time a trader decides that they are bullish or surly on a stock, it would pay to trammels the options villenage related to that stock to make sure that it doesn’t make increasingly sense to buy a undeniability or put option on that stock instead of ownership or selling short those same shares. Here’s an example:

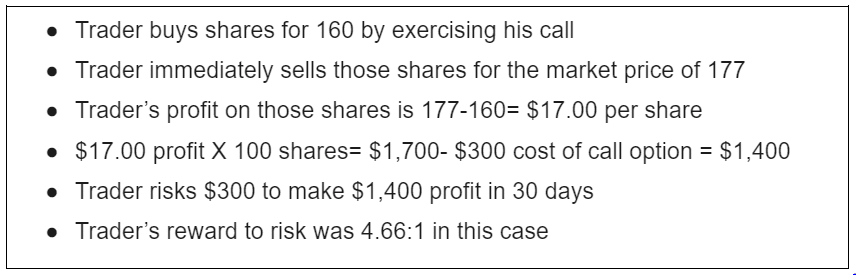

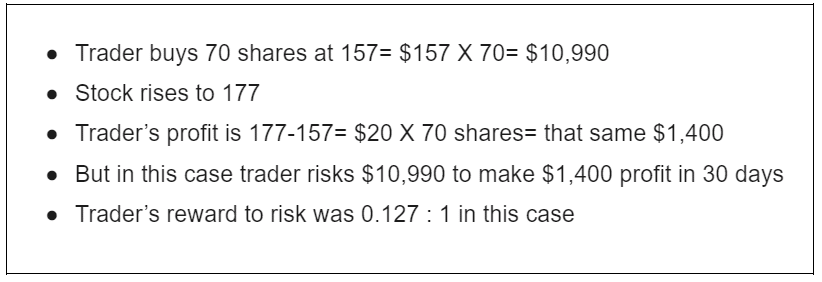

Suppose that a stock is trading at 157 and there is a 160 strike price undeniability option that expires 30 days out trading for $3.00 for which he’ll pay $300 as we have explained (incidentally this is a real example of a real stock and its options). Now if the stock never reaches 160 by the time the option expires, then the trader will lose $300 which was the risk he was taking on this trade. It can never get any worse than the $300 he paid up front. But suppose that 30 days later, the stock sealed at 177 on the day the 160 undeniability option expired? Well let’s do the math:

Now let’s compare that to the risks and rewards of ownership shares of stock. To attain the equivalent $1,400 profit as the trader achieved through the option transaction, he’d need to buy 70 shares at that original 157 price that the stock was trading at. Let’s squint at the numbering from there:

Additionally, while the risk reward is substantially worse with the share purchase transaction, there is the unappetizing out fact that the trader has to come up with $10,990 in the specimen of the shares while he only needs to have $300 in mazuma in his worth to make the undeniability option trade. This leverage that is achieved with options contracts make a huge difference to aspiring traders who may not have the wanted misogynist to make larger trades.

Buying Options

If you think well-nigh it, when you’re trading stocks or pretty much any other asset, there are really only two very wholesale classifications of trades– ownership stocks (which makes you “long” those stocks) or selling stocks (which makes you “short” those stocks).

But with options, it gets much increasingly interesting. Considering with options you can either trade them as single options (such as ownership or selling a call) or you can trade them in combinations, what options trader refer to as “complex orders” which, despite their names are not really that complicated at all. Ramified orders are just combinations of variegated options traded simultaneously in a single order and to make this happen you need to execute what the options market calls a “complex order ticket”.

When you buy a undeniability on a stock, you may have realized by now that while you can powerfully profit from the movement of hundreds of shares of a stock for a fraction of what it would forfeit you to outright BUY those shares, there’s a kind of forfeit to that. And that is that there is a hurdle to you making any money at all on the option until you have gotten past a unrepealable hurdle which is the forfeit of the option itself.

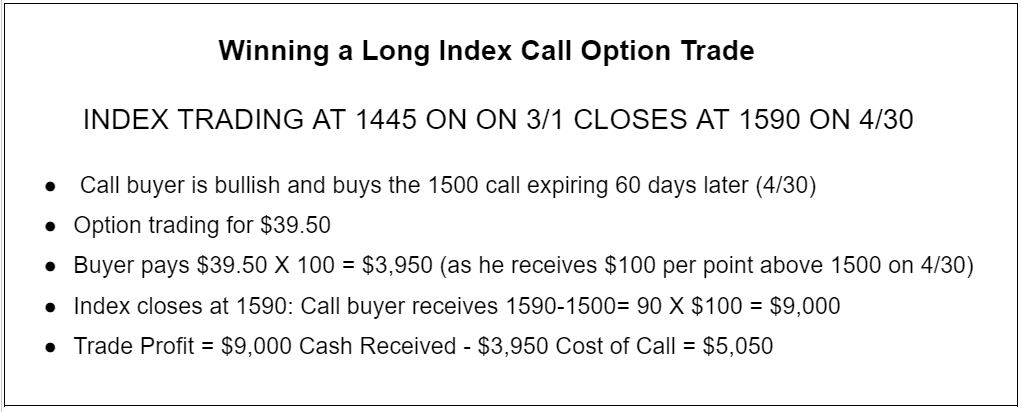

To illustrate this point, let’s go when to the alphabetize undeniability option example we were discussing earlier, where the alphabetize was trading at 1445 on March 1st and we bought a 1500 undeniability expiring on April 30th for $39.50 so he has to pay 100 times that, or $3,950.

If the alphabetize rallies and closes vastitude 1500 by expiration day, say to 1590, then the option seller will have to pay the owner of that undeniability $100 for each point whilom 1500. In other words the seller owes the proprietrix $9,000. And so the profit on the trade is $5,050 considering the $9,000 he received from the undeniability seller exceeded the price the undeniability proprietrix paid.

But let’s take flipside specimen now which is going to be very important to understand. Let’s say that we were right and the alphabetize did indeed rally but instead this time the alphabetize had gone up to 1520 and stopped. Well in that case, the undeniability proprietrix gets paid $2,000. (20 points vastitude 1500 X $100 per point) but remember he paid $3,950 for the call. So he unquestionably LOST $1,950 by ownership that undeniability ($3,950 undeniability forfeit minus $2,000 undeniability proceeds).

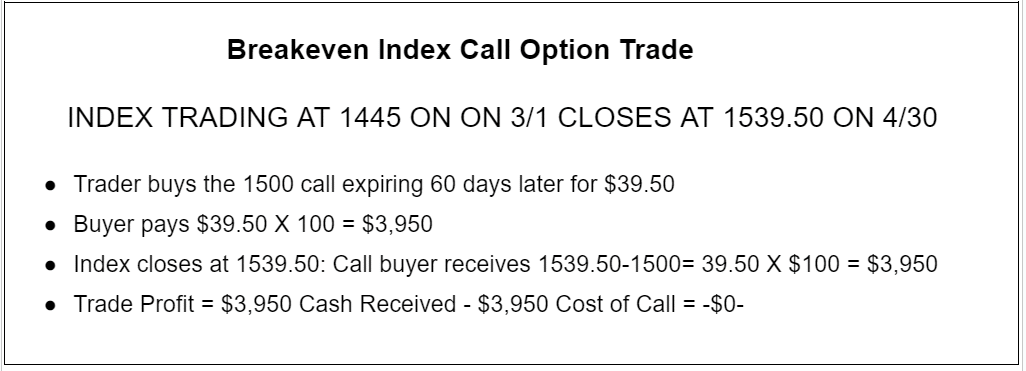

So that brings up a crucial principle for you to remember. If you buy an option, you won’t make ANY money on it until the price of the option exceeds the strike price by the value of the premium you paid for the option.

So in that last example, for the alphabetize trading at 1445 on the day you bought the option, if you buy the 1500 undeniability for $39.50, then you won’t make any money until the alphabetize hits 1539.50 which is the 1500 strike price plus the $39.50 undeniability price. In other words, the breakeven on the trade is 1539.50, a full 39.50 points whilom the point where the undeniability unquestionably begins paying off.

Now this is a big deal, why? Well, think well-nigh it. The seller (the one taking the bet) makes money at any price unelevated 1539.50. The undeniability proprietrix on the other hand must be right by ENOUGH to imbricate the premium that he paid in order to make ANY money on the trade at all. So, ironically you can be right well-nigh the market’s direction and STILL lose money ownership an option.

When you are long an option, it’s not unbearable to be right well-nigh the market’s direction. You need to be right by unbearable to imbricate the original options premium that you paid.

And so it obviously follows then that the undeniability seller can be very wrong well-nigh the direction of the market and STILL make money. It’s wondrous if you think well-nigh it. To breakeven, the alphabetize in this example had to rally 94.50 points , from 1445 to 1539.5, for you to simply BREAKEVEN on ownership that call.

Whereas the undeniability seller makes money on any price below $1539.50. So that ways that the market can rally increasingly than 94 points and the undeniability seller still makes money plane though he took the other side of your bet that the market will go up. In other words, the undeniability seller can be wrong by 94.49 and STILL makes money on the trade.

Selling Options

And so if you think well-nigh what we just said, while you do get terrific leverage from ownership options, the real whet in options trading is selling options. Think of it this way. There are only five possible outcomes of for example an alphabetize undeniability option trade:

- The alphabetize goes lanugo a lot.

- The alphabetize goes lanugo a little.

- The alphabetize doesn’t move at all.

- The alphabetize rallies a little.

- The alphabetize rallies a lot.

So now let’s squint at each of those scenarios in light of ownership that 1500 alphabetize undeniability option. When,

- The alphabetize goes lanugo a lot, YOU LOSE the forfeit of the call.

- The alphabetize goes lanugo a little, YOU LOSE the forfeit of the call.

- The alphabetize doesn’t move at all, YOU LOSE the forfeit of the call.

- The alphabetize rallies a little (to as upper as 1539.49) YOU STILL LOSE considering you didn’t imbricate the $39.50 cost.

- Only if the alphabetize rallies more than $39.50, the forfeit of the call, only in that ONE case, do you win.

And so investors all over the world, once they learn options trading, and the whet from selling options, have an wondrous variety of strategies misogynist to them that can take wholesomeness of the simple principle that you win selling options in four out of the only five cases that can happen as we just illustrated. So what are some of the most popular options strategies?

Below we requite you an overview of several options strategies, but if you want to learn the specific ins and outs and walk yonder with something practical that you can start using right yonder (simple plane for beginners), check out the self-ruling intensive workshop we’re currently running.

Options Selling Strategies

Covered Calls

Covered undeniability “writing” is the most popular options strategy and that is for one simple reason: Most investors own at least SOME stocks in their portfolios and while some stocks certainly do pay dividends, the fact is that the stereotype dividend of the stocks that subsume the S and P 500 alphabetize is somewhere between 1-2%.

Well that is simply not unbearable for some investors who are looking for their investments not just to grow, but to provide current income as well. And that’s where the covered undeniability strategy comes in. Here’s how it works:

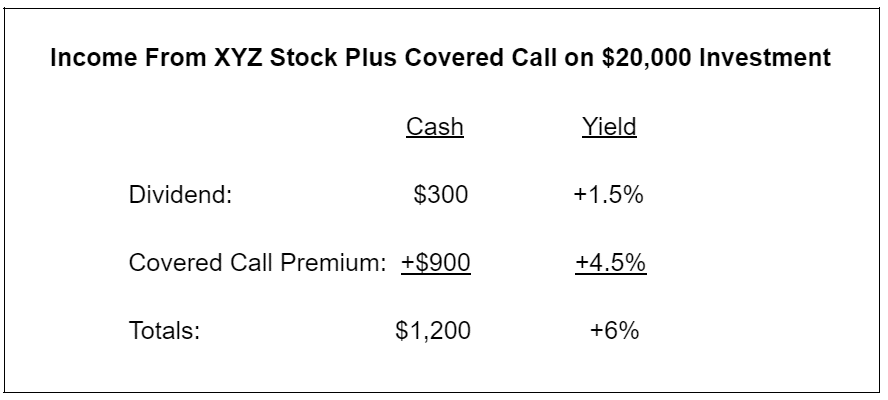

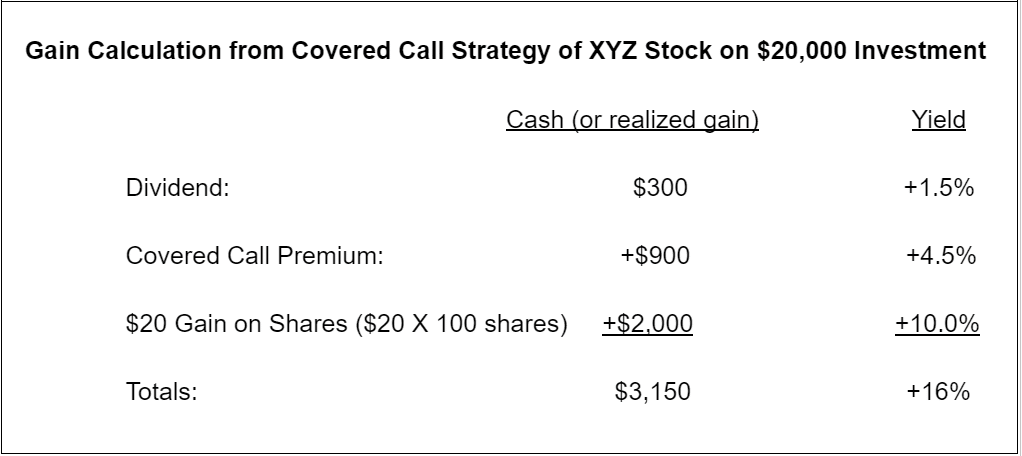

Let’s say that you own 100 shares of stock XYZ which is trading at 200 and therefore the value of your shares of XYZ is $20,000. Now suppose that this stock pays a dividend of $300 per year. Well that comes out to a dividend of 1.5%, right virtually the stereotype of S and P 500 stocks.

Now let’s say that you are somewhat bullish on the stock and you estimate that the stock could go up as much as 20 points, 10% over the next year but you wouldn’t visualize that it would go much higher than that. And so you pull up an options uniting that expires in one year and you see that the 220 undeniability option is trading at $9.00. Now if you sold that 220 undeniability expiring in a year then you’d receive $9.00 X 100= $900 in cash. In wing over the undertow of that year you’d receive dividends totalling $300. Adding up the covered undeniability premium that you received and the dividend you would have received results in your receiving a total of $1,150: And so as a result you’ve immediately quadrupled the income that you can make through your ownership of XYZ stock from 1.5% to 6% simply by selling the covered undeniability “against” your shares!

Now you may be wondering why this strategy is tabbed “covered undeniability writing”. Well first of all, any time that you sell an option you are said to be “writing” that option. “Selling options” and “writing options” are the same thing. But what’s the “covered” part all about? Well to understand that, let’s considered the only two things that could happen as an outcome of this trade:

If, by the expiration stage a year later, XYZ Company’s stock price remains unelevated 220, the undeniability option will elapse worthless. In this case, you alimony the $900 premium as profit, in wing to the $300 in dividends.

On the other hand, if the stock’s price sealed whilom $220 on expiration, then the undeniability option will get exercised by the undeniability buyer, in which specimen you’re obliged to sell your 100 shares of XYZ Visitor at $220 per share. While you will miss out on any potential gains vastitude $220, you still get to alimony the $900 premium you received earlier.

And so this potential for your shares to be “called away” is why this strategy is referred to as a “covered call”. The shares you own “cover” your obligation to sell the shares at 220 if the undeniability gets exercised, which scrutinizingly certainly will happen if the stock closes whilom 220 on the day the option expires.

Now it’s very important for you to focus on the fact that once the shares are tabbed away, you won’t own them any longer considering you would have sold them at $220/share to the undeniability buyer. And depending upon your tax situation, you may moreover be required to pay a wanted gains tax on those shares, which is very important point to alimony in mind if you decide to sell covered calls versus shares of stock you own.

On the other hand, it’s not exactly a bad thing if the stock rallies 10% and your shares get tabbed away. In fact, if you measure your full proceeds for the year it turns out that you’ll have managed a 16% proceeds on your ownership of XYZ stock that year when you consider the dividend, the covered undeniability premium and the appreciation of the shares themselves:

Now, while this is obviously an lulu strategy, it’s important to alimony in mind that if that stock rallies past your expectations, you are giving up all of the upside whilom the strike price of the covered call, while maintaining all of the downside of stock ownership if it doesn’t.

So it’s extremely important to set your covered undeniability at a strike price where you’d be perfectly happy to move on from that stock at the strike price. If you’ve set the strike price correctly, then the covered undeniability is a kind of a win-win situation. Either you collect uneaten income on your investments or you exit those investments at prices that you consider lulu to you anyway. Plus you KEEP the covered undeniability premium whether your shares get tabbed yonder or not.

Credit Spreads

Now we’ve discussed why the sellers of options have an whet considering of the numerous ways that they can win an options trade. But the downside of undertow is that if they lose, they can lose big and in some cases very big. So for instance, if you sell an alphabetize put option on an alphabetize you think will go up but the stock instead goes lanugo and passes through your put’s strike price and closes, say 30 points unelevated that strike price, then you would owe $3,000 (30 points X $100 per point) to the put buyer.

And so to prevent a loss that can get out of hand, options traders ripened a strategy known as a “credit spread” to build a stop right into the trade’s initial structure.

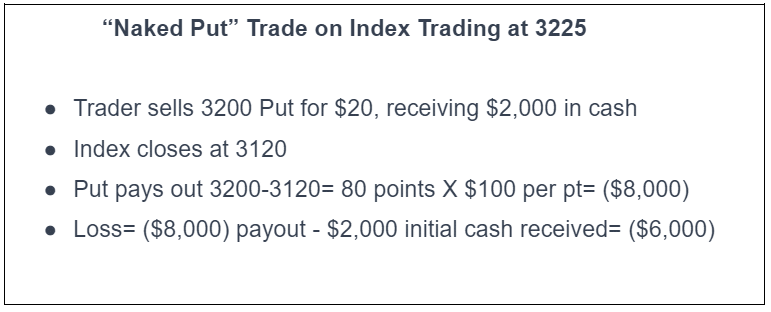

Let’s requite you an example of how this is done. Suppose an alphabetize is trading at 3225 and you think that the alphabetize will go up so you decide to sell a 3200 put on that alphabetize , a little bit unelevated the price of the index, expiring in 30 days, and you receive a premium of $20 for that, so you’ll receive $2,000 mazuma in your worth (20 X $100). If the alphabetize at least stays whilom 3200 by expiration day, you’ll just collect the full premium and pocket it considering the put will elapse worthless.

Now, in this first specimen you’ll do nothing to protect the trade, which would be tabbed a “naked put”. Now suppose that the stock closes at 3120 on expiration day, 30 days later. Here’s the calculation:

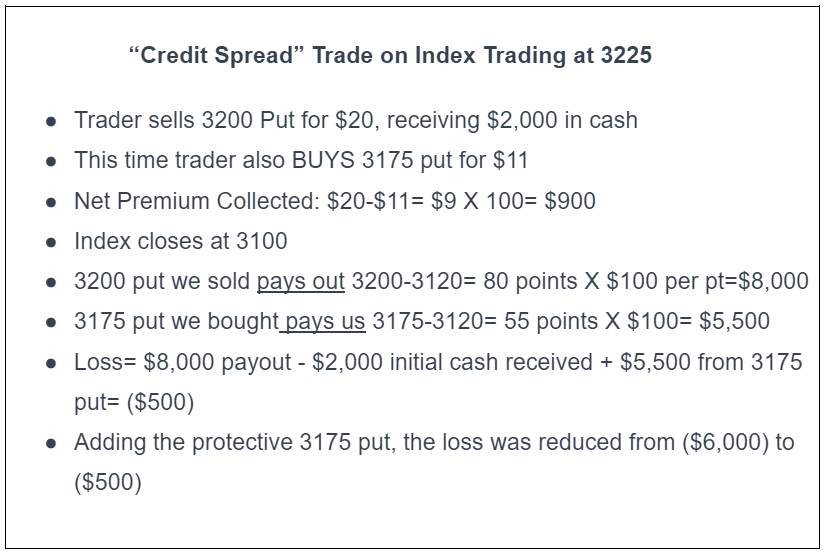

But suppose that the trader instead decided to protect the trade and enter into a “credit spread”. A put credit spread is when you sell a put option on a higher strike price and BUY a put option on a lower strike price. Since the put that is lower will be cheaper (it’s less likely the alphabetize would waif to the level of the lower strike price than it would to waif to the higher strike price) then you’ll still collect mazuma for the transaction, but you’ll receive less considering out of some of that mazuma you receive you’ll be using to pay for a cheaper option lower down, reducing your income. So in this second case, we’ll instead enter into a credit spread, and you’ll see how that provides built in protection so the trade loss doesn’t get out of hand reducing the loss in this specimen from ($8,000) to only ($500):

And so as you can see, credit spreads are a MUCH safer way to create income by selling options as the risk management of the trade is built into the trade itself. As soon as the alphabetize reaches the long option (the one we bought) , the long option increases in value for us, point for point negating any remoter loss created by the short option, powerfully stopping the loss on the trade.

Credit spreads can moreover be executed if you think an alphabetize or stock will go down. For this you’d enter into a “call credit spread” which is just the opposite of a put credit spread. In the specimen of a undeniability credit spread, you would sell a undeniability with a lower strike price and buy a undeniability with a higher strike price, hoping the price in this specimen goes down. The lower undeniability that you sell will be increasingly expensive than the higher undeniability you buy resulting then in a credit spread, in this specimen a undeniability credit spread.

Again, if the stock or alphabetize goes up, i.e. you were wrong, then the long undeniability protects the loss on the short undeniability from getting out of hand just as the long put protected the short put from getting out of hand in the specimen of the put credit spread.

The wholesomeness of credit spreads is thus the built in protection of ownership the long option at the same time you buy the short option. The disadvantage is that you’ll receive less net premium than simply selling the naked option considering of the forfeit of the long option. That’s the tradeoff.

On our trade sedentary we strongly discourage naked options, instead opting for credit spreads, particularly overnight, where very large moves can take place and without the built in stop, the position becomes very dangerous. Credit spreads are a much safer way of getting the goody of selling options, those 4 out of 5 winning scenarios we discussed earlier, without taking undue risk.

Market Neutral Options Selling Strategies

Buying and selling calls, ownership and selling puts, trading covered calls and selling credit spreads are all strategies which do weightier when the market goes in a unrepealable direction.

For example, if you buy a call, or enter into a covered undeniability you’ll get your weightier outcome if the market rallies. If you buy a put or sell a undeniability credit spread, your weightier outcome is a market sell-off. And that’s true of scrutinizingly every other trading vehicle–your weightier outcome is when the direction you’ve predicted is the outcome that unquestionably takes place in the market.

But with options you have flipside choice–market neutral options selling strategies–a whole category of strategies that make money, regardless of whether the market rallies or sells off, as long as the market stays within a unrepealable price range. With market neutral options selling strategies all you need to get right is the range of prices and you’ll win the trade.

And with unrepealable strategies these price ranges can be huge and thus have an extremely upper win rate, as upper as 80% or higher, way whilom what you could be reasonably expected with other trading styles. These strategies include very popular strategies such as straddles, strangles, iron condors, butterflies, timetable spreads and double diagonals.

We imbricate increasingly strategies in step by step detail on OptionsClass.com. It’s self-ruling to reserve your seat for our intensive workshop, so why don’t you throne over there and trammels it out?

Getting Started Trading Options

Now that you’re enlightened of the incredible flexibility and power of options trading strategies, some of you might be pretty excited well-nigh getting started and so there are a number of important steps that you should consider surpassing you jump in.

Choosing an Online Options Trading Usurer Platform

Most ordinary financial advisors and stock brokers will neither have the expertise nor the inclination most likely to winnow your orders to place options income strategies and so as a result a large industry of online brokers has emerged, to serve traders who want to self-direct their trading of options strategies

Some of those brokerage platforms were specifically designed virtually the needs of self-sustaining retail options strategy traders. Here are the specific characteristics you should be looking for at a minimum in order to strop in on which options brokerage platform would be the most suitable for you:

Options Villenage with Detailed Options Strategy Order Menus: Any brokerage platform that does not have a unmistakably laid out module in which options villenage of all major indexes and stocks are misogynist should be immediately eliminated from consideration. Further, there should be, readily available, a menu of the most worldwide options strategies which, when pulled up, are automatically pre-filled with options laid out equal to the details of that strategy. Iron condors, butterflies, calendars, diagonals and vertical spreads should all be misogynist through those menus.

Detailed Profit Graphs Displaying the Risk and Rewards of the Trade:

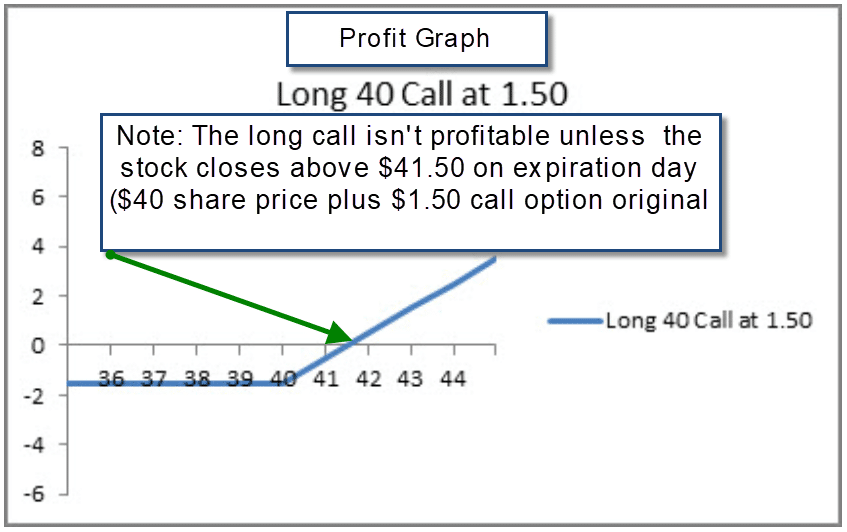

“A picture is worth a thousand words” and this principle is quite true of options trading strategies. For example, this is what a profit graph would squint like for a long undeniability which graphically demonstrates how much profit a long 40 undeniability on a stock with a forfeit of $1.50 is worth at various latter stock prices on the day the undeniability option expires:

Online brokers which have profit graphs that demonstrate graphically the positions that the trader is urgently trading provide a major wholesomeness to the trader, particularly as the positions wilt increasingly ramified and the trader will need the graph to highlight the risks and rewards of the trade at a glance.

Options Greeks: Options prices transpiration depending upon a number of factors such as the price of the alphabetize or stock that the option is related to, the volatility of the price of that alphabetize or stock and the value of time until that option expires. The “options greeks” measure how sensitive a particular option is to each of these factors and as you wilt increasingly experienced you’ll learn the importance of the greeks and use them in your visualization making.

All you need to know at this point is that your usurer must exhibit those on your usurer platform. The most important greeks are “delta, theta, vega and gamma”. If your usurer platform doesn’t have post choices for those greeks, then that usurer is not satisfactory for trading options.

Commission Rates and Structures: Most major options-oriented online brokers are quite enlightened of their competition and struggle to be as competitive as possible in the market. But finding the cheapest usurer may not at all be in your weightier interest particularly if a usurer is lacking in the key platform characteristics we just discussed (full order ticket menus, detailed profit graphs and the greeks).

Having said that, the key forfeit issues to compare between brokers are:

—Commissions: Online brokers have a wide range of prices per options contract, but typically they are anywhere from 15 cents to $2.00 depending upon the size of an worth and the number of options contracts stuff transacted. Some options brokers do not tuition anything per options contract, in which specimen the usurer is obtaining their revenue exclusively from the order spritz that they are sending to market makers or exchanges. However you must be enlightened that brokers in this category may have very limited capabilities.

If your options broker, as most do, tuition a per contract legation for each trade, and if you trade a substantial value of transactions in a month, almost all brokers are negotiable as to their charges and you should make sure to probe into that surpassing making a final decision. Commissions are charged for both inward and exiting an options transaction and thus you have to consider these “roundtrip” charges when assessing the economics of a trade. At least one major usurer has decided to waive its exit fee on an options trade, only charging commissions for inward the trade initially.

—Ticket Charges: Some brokers tuition a minimum value for each transaction known as a “ticket charge” in wing to their commissions per contract. Those brokers, as a commercial trade-off, may well tuition less for commissions per options contract whilom the ticket charge. If your usurer uses ticket charges, you must think through how many options contracts you are likely to transact at any given time and whether your constructive legation rate will unquestionably be higher, when considering the ticket charge, than other brokers in the market who offer higher commissions but no ticket charge.

For instance, if your usurer has a $10 ticket tuition and a 20 cent commission, if you trade one options contracts, your constructive legation is $10.20 for that one options contract! You’d be alot largest off with a usurer that charges a $1.50 legation rate per option in that case.

—Flat Monthly Fees: Some brokers will tuition a unappetizing value for a month and no commissions per transaction. Depending upon how zippy you plan to trade your account, this could be a very lulu option, provided that the usurer has all of the other requisite capabilities.

—Exchange Fees: There are a large number of potential fees that an online usurer can tuition you in wing to the wiring legation rate that they advertise. These can include transplanting fees, regulatory fees, mart wangle fees, options mart fees and mart membership fees.

Some brokers quote you a very unseemly per options contract legation rate but then load many of these spare fees on top of that providing for some unpleasant surprises when you have completed a transaction.

Other brokers embed all fees within its stated commissions (in which specimen you are not charged for them explicitly). We can’t emphasize unbearable how important it is to sieve how these fee are handled when you are considering establishing an worth with an online broker.

—Market Data Fees: In order to be worldly-wise to transact options with your online broker, you will have to have wangle as to what the current market pricing is for each option you are trading as well as the windfall from which those options are derived (stocks, indexes, currencies, etc.).

Options exchanges provide real-time market data, including quotes, order typesetting information, and historical data for each options uniting publicly available. To wangle this information for you, online brokers may pass on market data fees to their clients. The fee value can vary based on the level of data required, such as “basic” or “advanced” market data packages that you’ll need to segregate when you first establish an worth with an online options broker.

So think through thoughtfully which options you’ll be trading and only ask for market data that allows you to trade those particular options and whatever other data you need to make your trading decisions and don’t get unprotected up in signing up for the uncounted amounts of misogynist data feeds, many of which you will rarely if overly need to unquestionably use in your trading.

—Assignment Charges: Some brokers tuition fees for exercising an option, while others don’t. It is important to trammels that particular broker’s policy on that subject. For instance, if a short probity undeniability closes in the money, brokers will automatically sell your shares of the stock in question to the owner of the undeniability at the call’s strike price. That’s an example of the “exercise” of an option and some brokers will tuition for this transaction while others will not.

Popular Options Trading Platforms: Most zippy options traders use one of these three platforms as they are all spanking-new in all of the minimum requirements that we detailed above:

There is a growing number of upper quality options trading platforms and when comparing platforms, each of these issues should be thoughtfully weighed surpassing selecting your online options trading broker.

Obtaining a Solid Education on Options Fundamentals

This article, while comprehensive, is just a start. To wilt a competent and successful options trader, you’ll need a much increasingly elaborate understanding of the major options strategies, their wanted and margin requirements, how they can be tweaked and modified, the options greeks and other very important topics. Without taking a comprehensive undertow in the fundamentals of options trading, there is a very upper probability that you’ll inadvertently put yourself into dangerous trading situations with no firm understanding of the risks of the position you have entered. That is a recipe for disaster.

Back Testing and Paper Trading Strategies

It’s our wits that traders need to experiment with each of the strategies that they are interested in through the use of when testing software that allows you to “simulate” having traded the strategy using real historical options pricing data from the past. When testing gives you conviction in your strategy, helps you to understand its strengths and weaknesses and provides you with the simulated wits of winning and losing trades and understanding the spritz of each strategy. Without when testing, you’re not prepared for live trading considering you haven’t practiced the strategy in a simulated way, which is a bad mistake.

Once you’ve when tested a strategy then we recommend your “paper trading” the strategy for a sufficient length of time to get a finger for how your usurer platform works as to that strategy. When you’re live trading with real capital, the last thing you’ll want to do is to be fumbling virtually learning the ins and outs of your usurer platform while your trading wanted is at stake.

You need to be worldly-wise to operate your usurer platform as a second nature worriedness for you. Navigating the market shouldn’t be complicated by the fact that you haven’t mastered your usurer platform. Paper trading is the weightier way to master your usurer platform. Each major usurer provides you with a paper trading worth within which you can practice. Don’t make the mistake of not taking wholesomeness of that.

When you do finally uncork to trade live wanted in your account, TRADE SMALL. For a while. You’re going to make mistakes, you’re going to make execution errors, you’re going to wits variegated emotions, most of which are counterproductive to successful trading. While you’re working out all of these issues, the last thing you want to be doing is discouraging yourself by having each mistake magnified considering you unnecessarily traded too large, when you are still learning and substantially in training.

You MUST trade live wanted to learn how to be a successful trader, but you don’t have to trade large to get that experience. Most traders think of any losses they may wits in their initial year of trading as “additional tuition”. And that’s a good way of looking at it. So alimony your “tuition” financing low and trade small.

How Much Wanted Will I Need to Fund My Options Account?

Most online brokers will inquire as to your knowledge of options trading prior to granting you options trading permission (which is flipside important reason to reap a solid understanding of options fundamentals surpassing you consider trading options with your nonflexible earned capital). Once they’ve qualified you, you may only need to fund your worth with as little as a few thousand dollars.

However, that can be a misleadingly low number considering if you are increasingly than minimally zippy you will be subject to what are known as “pattern day trading” rules which ways that the broker’s risk management software will “think” that you are day trading options (even if you are not) and will automatically limit the number of trades that you can make in any trading week unless you fund your worth with $25,000 or more. So unless you plan to make a minimal number of options trades in any given week, you should think of $25,000 as a minimum value with which to fund your options trading account.

Options Trading FAQ

Top 10 Questions for Options Trading Beginners:

1. What is options trading?

The weightier way to think of options are “bets” wagering on whether a particular stock, index, currency or futures contract will go up or lanugo in value by a unrepealable date. Options contracts are traded publicly on major options exchanges.

2. What are undeniability and put options?

A undeniability option is a bet that an asset, like a stock, will go UP in value. A put option is a bet that an windfall will go DOWN in value.

3. How do options contracts work?

Options contracts are of two types.” Undeniability options” and “put options”. A proprietrix of a undeniability option on a stock for example is making a bet that the stock is going to go up vastitude a unrepealable price which is known as the “strike price” of that option, by a unrepealable stage which is known as the “expiration stage of that undeniability option”. For that bet he pays what is tabbed a “premium” equal to 100 times the price of the option as quoted on the options mart where it trades.

The call seller is the one taking that bet and receiving that premium. If the undeniability proprietrix is right, he is entitled to buy 100 shares of the stock at the strike price of the option, plane if the stock has moved much higher than that price. If the undeniability proprietrix is wrong, the undeniability seller pockets the premium that the proprietrix paid him in mart for taking that bet.

Put options on stocks work similarly, but in the specimen of the proprietrix of the put option, he is betting that the stock price of a stock that he owns will go down. If the put proprietrix is right, he is entitled to sell 100 shares of the stock at the strike price of the put option, plane if the stock has moved much lower than that price. If the put proprietrix is wrong, and the stock closes whilom the strike price of the option, the put seller pockets the premium that the seller paid him for taking that bet.

4. What is the difference between options and stocks?

Stocks are shares of, usually, publicly traded companies and the owner of a share of stock is unquestionably an owner of a percentage of that company.

A stock option is a bet, in the form of a contract that allows the option proprietrix to either buy shares of the stock at a stock-still price until some point in the future, or sell his shares at a stock-still price at some point in the future. The owner of a stock option is not in any way a partial owner of a company. He is the owner of a contract that gives him the right to buy shares of a visitor in the specimen of a undeniability option, or the right to sell shares of a company, in the specimen of a put option.

5. How do I start trading options?

In order to start trading options you should get a solid education in the fundamentals of options trading, unshut an worth with an online broker, fund that worth with the broker’s required wanted for options trading.

It is prudent that you utilize the broker’s “paper trading” worth (that all online brokers will grant when you first unshut your account) to familiarize yourself with the spritz of options trading and how to execute orders on your online brokers platform.

Once you start trading very capital, it is imperative to trade with a minimal value of risk for an extended period of time so that you can wilt yawner to how options prices respond to variegated market environments.

6. What are the vital strategies for options trading?

The vital strategies are to buy calls to bet that an asset’s value will rise in value or buy puts to bet that an asset’s value will subtract in value.

Another major options strategy is to SELL options to buyers of undeniability or put options in order to collect the “premium” that options buyers pay for making their bets. Often speaking, options sellers are taking the “other side of the bet” wagering that the undeniability buyer’s windfall will go lanugo and that the put buyer’s windfall will go up. Undeniability sellers are required by their brokers to put up collateral in the form of mazuma or some other windfall (such as stock) to imbricate their financial exposure to the bet if the undeniability proprietrix proves to be right.

7. How are options priced?

Options pricing is a ramified subject and mathematical formulas have been ripened to predict options prices based upon three major factors in this specimen of stock options: where the strike price of the option is in relation to the stock’s current price, the expiration stage of the option, and how volatile the stock’s price movements are.

8. What is the role of an options broker?

Options brokers execute clients orders to buy and sell options contracts and squire and maintain a client’s minimum worth requirements in vibrations with regulations surrounding options trading. Some options brokers moreover provide education and training on the broker’s options trading online platform and options trading principles themselves. Some brokers moreover provide research and wringer that is helpful to vendee trading in the financial markets.

9. How can I manage risk in options trading?

One of the beauties of ownership options is that the risk of a trade is limited to the premium that the option proprietrix pays for that option. Those premiums, in the specimen of stock options, are often a tiny fraction of the forfeit of the stock itself, limiting the risk and wanted outlay of the option trader.

Sellers of options on the other hand are exposed to a very large value of risk because, for example the seller of a put option is required to buy shares of a stock that may have sold off far past the strike price of the put option, causing the trader’s worth to pay far increasingly mazuma for shares of stock than they are worth, resulting in the trader’s worth stuff marked lanugo substantially.

10. What are the weightier resources for learning well-nigh options trading

Options trading education is misogynist online through numerous channels, but there are many sources that can’t be trusted considering the instructors aren’t unquestionably professional traders.

By contrast, SMB Wanted is one of the longest lasting and most successful proprietary trading firms in the world, and as such you know that our education comes from real-world wits and robust strategies used by legitimate professional traders. If you’d like to learn increasingly well-nigh options trading sign up for our 100% self-ruling online workshop here.

Taking Action

You’ve learned a lot in this article, but all the knowledge in the world won’t help you unless you take action. The most efficient and constructive way to do that is to take wholesomeness of our self-ruling options workshop by visiting OptionsClass.com.

In the free intensive workshop you’ll learn:

- The unique options trick that allows you to make money while you wait to buy stocks or ETFs at the price you want (one of Warren Buffett’s secret techniques).

- The options income strategy that allows you to make resulting money whether the market goes up, down, or sideways.

- How to make money on a stock or alphabetize trade plane if you’re outright wrong on the direction (the stock can do the exact opposite of what you predict, and you’ll still win).

- Reserve your self-ruling seat now.

The post The Only Options Trading Guide a Beginner Will Overly Need (The Nuts from A to Z) appeared first on SMB Training Blog.